There’s no longer any question that banking has hit the digital tipping point. According to a 2019 American Bankers Association (ABA) survey, the banking channels used most often by consumers are online (37%) and mobile apps (36%), with bank branches now in third place at 17%. But before we declare the branch model is doomed…take note: a 2018 Celent survey found that 77% of consumers prefer visiting a branch to discuss a lengthy topic, 63% prefer a branch for investment advice, and 51% opt for a branch to open a new deposit or credit card account. And Deloitte’s Global Digital Banking Survey revealed that branch experience influences customer satisfaction more than mobile or online channels.

So while banks are investing more and faster in digital platforms, they are also looking to solve the puzzle of next-gen branch banking. Here are 3 ways that banks can reinvent their human channels to perform effectively in a digital world.

Reduce the overall number of branches, but look to open branches to expand reach.

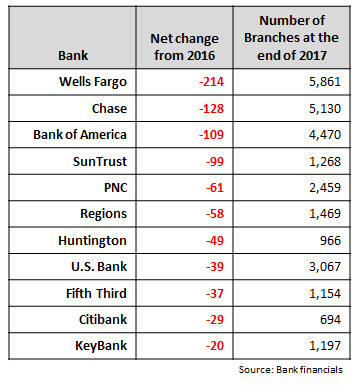

Over the past decade, there has been a net decline of more than 13,000 bank branches in the U.S.

The pace and extent of each bank’s branch reductions have varied widely, driven largely by growth opportunities in footprint geographies and competitive intensity:

- In April 2019, midwest-focused U.S. Bank announced plans to trim up to 15% of its branches by the end of 2021 as it pursues a digital-first strategy.

- Wells Fargo’s branch strategy maintains significant branch presence in attractive markets, while aggressively reducing branch counts in other markets.

Lower branch density has reduced the cost of entry into some new markets. While many banks are cutting their overall branch numbers, they are also opening branches in targeted strategic markets.

- In 2018, Chase announced plans to open 400 branches in 15-20 expansion markets, including Boston, Washington, D.C. and Philadelphia. As a result of this expansion, Chase’s branch network coverage will rise from 69% to 93% of the U.S. population.

- Similarly, though Bank of America has reported a net reduction of more than 750 branches over the past five years, it has also opened 200 new branches, with another 400 expected to open over the next three years in markets like Cincinnati, Cleveland and Pittsburgh.

- To achieve its ambition of national presence, PNC has targeted new markets with a digital-first strategy supported by a thin branch network. It recently opened branches in markets like Dallas and Kansas City, and reports these new branches are generating deposits at five times the pace that the bank would expect for a de novo branch in its legacy markets.

Reimagine branches.

Branches have long since begun transformation from service centers to…well, something else. Some banks have set an immediate course for sales, driving service transactions to smart ATMs and contact center hotlines and pulling real estate from tellers to sellers. Other FIs have redesigned select branches or entire networks as everything from experiential attractions to coffee houses to community centers.

Universal trends are fewer square feet and more open space. Matching those changes, branch headcount is lower and skill levels higher. From the nation’s largest banks to some of the smallest, branches are being reinvented.

- On the regional end of the scale, 132-branch Berkshire Bank is introducing new “storefronts” in greater Boston. No tellers, but if you need to make a conference call, you’ll find free co-working spaces and event rooms. Just be prepared to have a “needs assessment” with your friendly Berkshire banker coming or going.

- Global bank, HSBC deployed “Pepper,” a humanoid robot in New York City, Seattle, Beverly Hills and Miami. Likely more of a marketing play than a scalable technology innovation, the bank claimed that the presence of Pepper boosted business by 60% in New York alone.

- Chase–ever practical–launched Digital Account Opening in branches, so the technology can handle the busywork leaving bankers time for providing advice (read selling). And Bank of America is in the middle of a six-year plan to renovate 2,800 branches, flat-out taking humans out of many, leaving only machines.

- Oregon-based Umpqua takes a contrarian view that people want to bank with people, and invites branch traffic with cookies, chocolate coins, movie nights and marketplaces where small business clients can share their wares with retail customers.

Make physical and digital work together. Human matters.

Intuitive technology is good for reducing cost, but humans are better at driving sales, creating relationships and building loyalty. Beyond the small businesses and aging boomers who still prefer the corner bank to the cool app is the reality that in “money moments that matter,” people turn to people–whether it’s in a branch or a contact center. But those humans must be consistently positive, empathetic and “know” everything that the technology channels know. Winning banks will:

- Design an onmichannel approach that enables customers to use the channel they choose with consistent experience

- Recognize the brand value and acquisition horsepower of branch networks

- Give your customers great digital experiences, but power your human channels with the best in technology and insights to make the most of those moments that matter