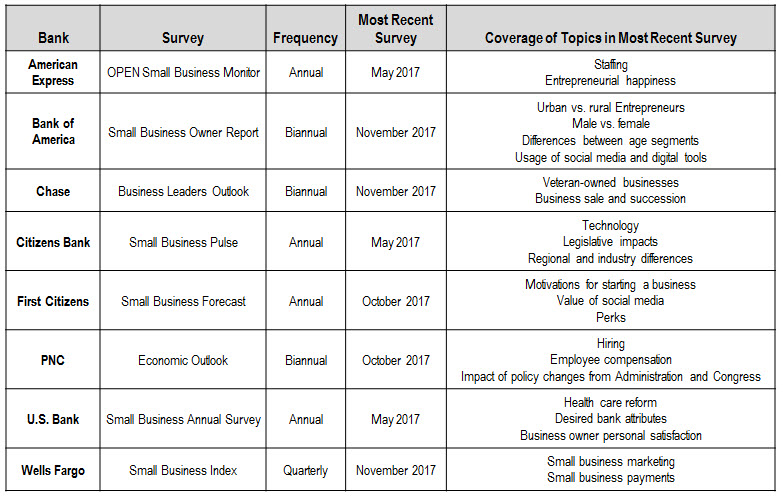

In May 2017, EMI published a blog that discusses how banks use surveys to build small business engagement. In that blog we reported that many leading banks publish recurring surveys that track general business optimism as well as key challenges and opportunities. In addition, banks also carry surveys that cover specific topics on a one-off basis. The following table looks at the topics covered over the past six months:

The banks cover these topics of interest to achieve a number of objectives, including:

- Raising general awareness of the bank and affinity among small businesses

- Positioning the bank as a small business banking thought leader

- Communicating their understanding of the changing issues impacting small businesses

- Highlighting their areas of strength

- Differentiating the bank from its competitors

In fact, the desire for differentiation is leading banks to conduct surveys on specific small business sub-segments or on specific product areas. Recent standalone surveys of this type include:

- U.S. Bank surveys of Asian-American small business owners (October 2017) and Hispanic small business owners (October 2017)

- Surveys by both Bank of America (September 2017) and American Express (November 2017) on women-owned businesses

- Bank of America Small Business Payments Spotlight (October 2017)

- American Express Small Business Saturday Consumer Insights Survey (November 2017)

The proliferation of small business surveys that cover specific topics of interest indicate that they are effective tools in helping banks build awareness and engagement with their small business clients and prospects.