The FDIC recently published detailed branch and deposit data for different geographic levels for all U.S. banks. EMI’s analysis of this data revealed the following trends:

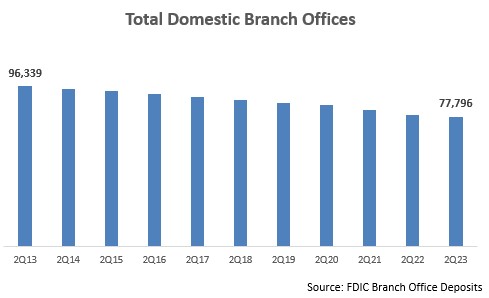

There is a continued (but slowing) decline in the number of bank branches. Over the past 10 years, the total number of domestic branches for FDIC-insured institutions declined by almost 24% to fewer than 78,000 branches. This equates to an annual average decline of 2.1%. In 2Q21 and 2Q22, the y/y rate of decline exceeded 3%, but this slowed to 1.7% y/y to the end of June 2023.

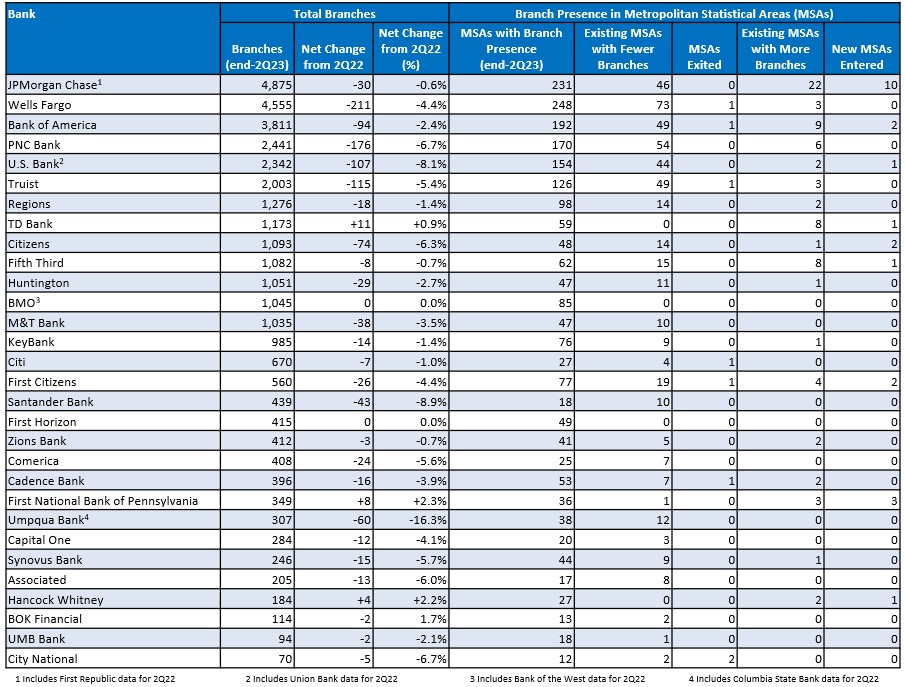

Some of the largest banks had the strongest percentage declines in branches. Our detailed analysis of 30 leading banks (see below) found a 3.1% y/y decline in branches (from 35,039 to 33,920) at the end of 2Q23. However four banks with networks of more than 2,000 branches reported declines of more than 4%: Wells Fargo (-4.4%); PNC (-6.7%); Truist (-5.4%) and U.S. Bank (-8.1%). Santander Bank reported the largest percentage decline (-8.9%).

Some banks are growing their branch networks. While the overall trend has been for banks to trim their networks, some banks are maintaining or even growing their commitment to this channel. TD Bank grew its network by 11 branches, adding branches in 8 existing markets, as well as opening its first branch in The Villages, FL. Following the collapse of its planned merger with First Horizon earlier this year, TD announced plans to open 150 U.S. branches by 2027 with a focus on Southeast markets.

Banks are maintaining their presence in the vast majority of their markets. While banks are reducing branch density in their existing markets, few are completely leaving these markets. Seven of the 30 banks exited a market over the past year, but only one left more than one market: City National Bank closed its branches in both Reno and Carson City, NV.

Branch closures were spread across many existing markets. Overall, the 30 banks closed branches in 22% of their existing markets, through several had higher percentages of existing markets impacted by closures, including Santander Bank (56%), Truist (39%) and PNC (32%).

Banks concentrated their reductions on markets with the largest branch networks. Banks reduced branch densities in many of their main markets, enabling them to cut costs while maintaining a significant presence. Although more than a third of Wells Fargo’s branch reductions took place in just 8 markets, each of those markets continues to have more than 100 branches.

Some banks are opening new branches in existing markets. The 30 banks increased branch numbers in 4% of existing markets, led by TD Bank (increased branch numbers in 14% of their existing markets) and Fifth Third (13%), who are both expanding their presence in key southeastern U.S. markets. JPMorgan Chase increased branch numbers in 22 markets (10% of its existing markets), including Washington (+11 branches), Minneapolis (+9), Kansas City (+7) and St. Louis (+7).

J.P. Morgan Chase is leading the way in market expansion. Over the past year, the bank opened branches in 10 new markets, including Buffalo and Virginia Beach (4 new branches in each market). This is part of a longer-term strategy to grow its branch footprint: the bank reported at its 2023 Investor Day that its population coverage rose from c. 60% in 2017 to c. 80% in 2022, with the bank now aiming for 85% population coverage.

Now that Congress and the Administration have agreed on a $310 billion deal to replenish the Paycheck Protection Program (PPP), banks are scrambling to help small businesses apply for this additional funding. At the same time, banks are providing information to small business clients on direct reliefs and channel availability, as well as tips to deal with the COVID-19 pandemic.

The enormity of the challenge facing small businesses and the economy as a whole defies description. No communication can overcome this burden. But silence is not an option and messaging matters. It’s critical to communicate effectively with small business clients during this pandemic.

Develop a multi-faceted response. The PPP is vital for many small business owners, but many banks have only been providing information on how to apply for PPP. This means they are missing other opportunities to engage with and help small business owners, many of whom are struggling with day-to-day operational issues. Consider offering additional information on supports available to small businesses, and advice on how to navigate through the pandemic.

Best practice: PNC has developed a range of content to help small businesses deal with the crisis, including “Four Ways Small Businesses Can Navigate During Times of Uncertainty” and “What to Do When Cash Flow Slows.”

Create a connection. Messaging on coronavirus response must be both clear and empathetic. This is particularly important in headlines and topline statements on how the bank is supporting its small business clients.

Best practices: Citizens Bank and KeyBank both use the theme of “We’re in this together” for their coronavirus information.

Communicate information clearly. To ensure that small business clients are directed to key information and not overwhelmed by detail, focus on strong copywriting and editing, as well as using layout and navigation tools to help readers quickly find what they need.

Best practice: Santander Bank uses red type, spacing, headings, and bullet points to effectively organize its COVID-19 response information.

Best practice: TD Bank uses tabs on its website to direct small businesses to information on its own customer assistance program, SBA PPP Loans, and other relief options.

Provide guides and tools. Many banks have developed tools (such as online forms, FAQs, guides and checklists) to aid small businesses in understanding support and options available to them,and to apply for funding

Best practice: Huntington Bank has published a series of FAQs to address various aspects of the PPP program, including general questions, eligibility and application information.

Best practice: Umpqua Bank integrated a well-designed application form into its CARES Act Paycheck Protection Program information page.

Consolidate all information into a single resource center. Develop standalone portals or resource centers to retain all coronavirus-related information in a single location. This enables you to maintain a consistent tone in coronavirus messaging, avoid any client confusion, and better manage the process of providing updates.

Best practice: Citizens Bank operates a dedicated COVID-19 Resource Center, with links to services and resources, details on financial hardship relief assistance and a message from the bank’s CEO.

Embrace multiple communications channels. Use the numerous channels – branch, phone, website, social media – at your disposal to provide updates and directly engage with small business clients.

Best practice: PNC directs clients to dedicated toll-free numbers for different product categories; some numbers are operational 24×7.

Update information regularly. Many banks provided initial information on their COVID-19 response, but they have not provided regular and comprehensive updates, a critical failing in this extremely dynamic environment.

Best practice: Bank of the West publishes regular updates in videos featuring the bank’s CMO Ben Stuart.

Consumer transition to digital channels for everyday banking needs reached a tipping point in 2019. A recent ABA/Morning Consult survey found that 73% of Americans access their bank accounts most often via online (37%) and mobile (36%) channels. And more consumers are also now embracing digital channels for more financial activities, from buying new financial products and services to securing financial advice.

Responding to this trend, and the march towards improved efficiency, many financial providers are “chasing digital” from the boardroom to the back office. Some take an incrementalist strategy, doggedly adding functionality or product sets to online and mobile platforms. Some have bought or built standalone digital brands, or layered digital over thin branch networks out of footprint. And, of course greenfield revolutionaries continue to dive in to the fray. We look at four models that are working, and what marketing mix and methods matters most for each.

All banking roads lead to digital these days–which path is right for you?

National Banks Double Down on the Human-Digital Model

Banks with a national or quasi-national branch footprint and strong brand equity – including JPMorgan Chase, Bank of America and Wells Fargo – have focused less on driving digital deposit growth to date and taken evolutionary approaches to driving digital banking. Take Erica, for example, Bank of America’s AI-based personal assistant, launched in June 2018. Over the past 18 months, Bank of America has systematically expanded Erica’s capabilities, and methodically marketed it to customers. The platform recently reached 10 million users. The same month that Erica appeared, JPMorgan Chase launched Finn, a standalone digital banking platform designed to appeal to a younger demographic. Just one year later Finn was shut down in a “fail fast” move, and Chase now appears to be doubling down on both digital banking evolutionary enhancements and selected branch expansions.

These national banks have significant technology budgets, and they are using them to launch a steady stream of new digital banking capabilities, citing increased customer satisfaction, higher share of wallet and reduced attrition. Bank of America calls it “moving from digital enrollment to digital engagement.”

Bigger banks are also pointing marketing budgets at digital adoption. We see an increasing number of multi-channel programs promoting digital capabilities and driving trial, including broadcast advertising, online banking ads, in-branch demos, social media and more.

While technology and marketing budgets are driving results, national banks will benefit most from a long-term channel-agnostic approach that emphasizes the strength of physical channels in acquisition, advice and complex product sales. Treating the digitization of human channels with the same attention as customer capabilities will yield higher return for banks with big branch horsepower. Too often, the glamour and appeal of digital banking pushes training and tooling for branch and contact center staff down the annual project queue. Putting next-best product predictors, automated diagnostic tools and intuitive digital solution finders in the hands of client-facing humans has high ROI.

Regional Banks Expand Reach with Digital Models

Regional banks by definition are deep in their footprints, and see digital banking as a lower-cost geographic expansion play–in some cases supported by a thin physical network. This strategy typically starts with a high-yield savings account, then adds other products (e.g., checking, lending) and digital tools. Whether regionals find the equation to manage cost of acquisition, driven by high marketing costs and NIM pressure, will be key to delivering on the promised cost-efficiency plan.

Regional banks leading the digital bank charge include:

Citizens Bank: With national aspirations and low brand equity outside of its Northeast and Midwest footprint, Citizens Access offers this high-performing regional a “nationwide digital platform.” Launched in June 2018, Citizens Access had generated $5.8 billion in new customer deposits by the end of 2019. Next up, Citizens is talking expansion into business savings and digital lending.

PNC expanded its digital banking capabilities in October 2018, leading with a high-yield savings account. Like several others, PNC has articulated a “thin network” strategy–combining digital bank investments with lean branch buildout in a few high-opportunity markets (in PNC’s case, Kansas City and Dallas).

Union Bank: Another thin network player, MUFG Union Bank introduced a “hybrid digital bank” under a separate brand, PurePoint Financial, in 2017. With a NYC headquarters setting it apart from Union Bank’s West Coast heritage, the PurePoint positioning emphasizes its parent Mitsubishi’s size and global scale, and its 22 locations in Florida, Texas and Chicago. The requisite high-rate savings and CD offers are complemented with heavy financial education.

Santander Bank recently announced plans for a digital bank later this year, but unlike others, plans to pilot in its Northeast footprint.

Monolines, Specialized Lenders Turn to Digital for Diversification

This category of financial firms includes dedicated credit card issuers with no branch presence (e.g., American Express, Discover), as well as banks with a strong heritage in card or other lending and who have a limited retail banking footprint (e.g., Capital One, Citi, Ally, CIT).

Marketing Priorities and Challenges:

These banks have national lending franchises and strong brand equity. However, as their brands are often strongly associated with their lending operations, a key marketing challenge will be to expand consumer awareness of the bank as a provider of other banking and financial solutions.

They will need to focus on data analysis, targeting, offer development and messaging to effectively cross-sell deposits and other products to their existing card/other loan client bases. This approach will also involve significant cooperation among different business units. Citi has been at the forefront in marketing deposit accounts to its 28 million credit cardholders and generated $4.7 billion in digital deposits in the first 9 months of 2019: two thirds of the deposits came from outside its six core banking markets.

Fintech Disruptors Continue to Emerge

Widespread availability of venture capital and private equity money continues to fuel a spate of fintechs entering the market, including Chime, N26, Radius Bank and Monzo. Many predecessor neobanks have been challenged to achieve scale, as the cost of customer acquisition in digital banking has continued to rise. Fintechs typically partner with a small bank or servicer to offer deposits, but some (such as Varo Money) are now looking for independent bank charters.

Marketing Priorities and Challenges:

The digital bank upstarts tend to appeal to younger age segments who are both more accustomed to using technology to manage their financial needs and less loyal to traditional banks. These companies need to clearly understand how these younger segments consume media and make financial decisions and tailor their marketing investment and messaging accordingly.

As “new kids on the block,” fintechs will need to develop solutions and marketing to differentiate themselves from both traditional banks and other challenger banks.

The design and ongoing review of the digital user experience is critical, as this is the only platform consumers will have to interact with the bank. Some digital banks are not even offering phone-based customer service.

While challenger banks have a number of advantages over traditional banks (such as higher rates on deposits), there are other areas where these newcomers are seen as inferior (for example, a recent Kantar study found that 47% of consumers completely trust traditional banks, but this falls to 19% for challenger banks). Challenger banks need to develop messaging to directly address these areas of vulnerability, and communicate consistently through all consumer touchpoints.