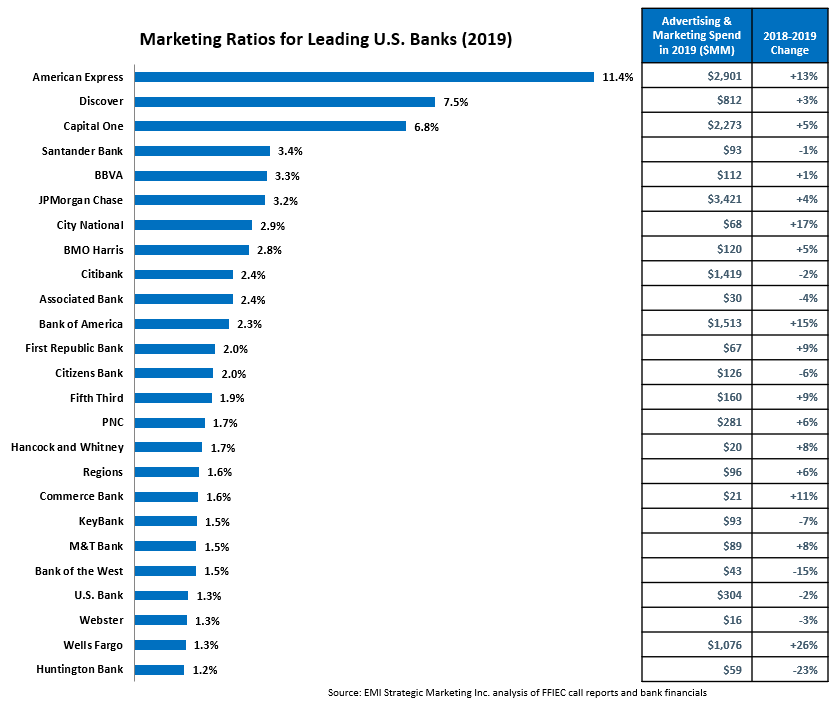

EMI’s annual analysis of marketing expenditure for 25 leading U.S. banks reveals that they grew marketing spending by 7% in 2019 to $15.4 billion. This rate was down from the 13% growth between 2017 and 2018.

The banks’ marketing ratio (defined as advertising and marketing spend as a percentage of net revenue) has risen steadily in recent years, growing 18 basis points (bps) to 2.92% in 2018, and by an additional 21 bps to 3.13% in 2019.

The chart below summarizes marketing ratios, marketing budgets and y/y change in marketing spending for these 25 banks.

The following are some additional takeaways from our bank marketing spend analysis:

16 of the 25 banks increased their marketing spending in 2019, with 5 increasing their budgets by more than 10%.

6 banks invested more than $1 billion in advertising and marketing. Wells Fargo joined this group for the first time in 2019, with marketing spending rising by 26%, driven in large part by the launch of the ‘This is Wells Fargo’ integrated marketing campaign in January 2019 . It has invested strongly in advertising in recent years as it seeks to rebuild its reputation following the fallout from fake account and mortgage mishandling scandals.

11 banks increased their marketing ratios in 2019, with 6 of these growing the ratios by more than 10 basis points. The largest rise was reported by Bank of America, whose 15% increase in its marketing spend led to a 38 bps rise in its marketing ratio (to 2.3%).

Banks that do not have branch networks and have national credit card franchises (American Express and Discover) had the highest marketing ratios. Capital One’s credit card bank charter – Capital One Bank (USA), National Association – had a marketing ratio of 10.3% in 2019, while its retail banking charter – Capital One, National Association – had a ratio (3.2%) more in line with peer regional banks.

It is almost impossible to project bank marketing spending for 2020, given the impact of the coronavirus pandemic on the U.S. economy in general, and the banking sector in particular. In the short term, marketing budgets will trend downwards as bank revenues are impacted by decreased economic activity. However, unlike the 2018-09 Financial Crisis, the country’s fundamentals were strong heading into this disruption, which increases optimism that the economy can recover quickly once the pandemic abates. This may lead to a robust bank marketing spending in the second half of 2020. What is more clear is banks will continue to shift their marketing budgets from traditional media (e.g., TV and print) to digital and other nontraditional media.

Consumer transition to digital channels for everyday banking needs reached a tipping point in 2019. A recent ABA/Morning Consult survey found that 73% of Americans access their bank accounts most often via online (37%) and mobile (36%) channels. And more consumers are also now embracing digital channels for more financial activities, from buying new financial products and services to securing financial advice.

Responding to this trend, and the march towards improved efficiency, many financial providers are “chasing digital” from the boardroom to the back office. Some take an incrementalist strategy, doggedly adding functionality or product sets to online and mobile platforms. Some have bought or built standalone digital brands, or layered digital over thin branch networks out of footprint. And, of course greenfield revolutionaries continue to dive in to the fray. We look at four models that are working, and what marketing mix and methods matters most for each.

All banking roads lead to digital these days–which path is right for you?

National Banks Double Down on the Human-Digital Model

Banks with a national or quasi-national branch footprint and strong brand equity – including JPMorgan Chase, Bank of America and Wells Fargo – have focused less on driving digital deposit growth to date and taken evolutionary approaches to driving digital banking. Take Erica, for example, Bank of America’s AI-based personal assistant, launched in June 2018. Over the past 18 months, Bank of America has systematically expanded Erica’s capabilities, and methodically marketed it to customers. The platform recently reached 10 million users. The same month that Erica appeared, JPMorgan Chase launched Finn, a standalone digital banking platform designed to appeal to a younger demographic. Just one year later Finn was shut down in a “fail fast” move, and Chase now appears to be doubling down on both digital banking evolutionary enhancements and selected branch expansions.

These national banks have significant technology budgets, and they are using them to launch a steady stream of new digital banking capabilities, citing increased customer satisfaction, higher share of wallet and reduced attrition. Bank of America calls it “moving from digital enrollment to digital engagement.”

Bigger banks are also pointing marketing budgets at digital adoption. We see an increasing number of multi-channel programs promoting digital capabilities and driving trial, including broadcast advertising, online banking ads, in-branch demos, social media and more.

While technology and marketing budgets are driving results, national banks will benefit most from a long-term channel-agnostic approach that emphasizes the strength of physical channels in acquisition, advice and complex product sales. Treating the digitization of human channels with the same attention as customer capabilities will yield higher return for banks with big branch horsepower. Too often, the glamour and appeal of digital banking pushes training and tooling for branch and contact center staff down the annual project queue. Putting next-best product predictors, automated diagnostic tools and intuitive digital solution finders in the hands of client-facing humans has high ROI.

Regional Banks Expand Reach with Digital Models

Regional banks by definition are deep in their footprints, and see digital banking as a lower-cost geographic expansion play–in some cases supported by a thin physical network. This strategy typically starts with a high-yield savings account, then adds other products (e.g., checking, lending) and digital tools. Whether regionals find the equation to manage cost of acquisition, driven by high marketing costs and NIM pressure, will be key to delivering on the promised cost-efficiency plan.

Regional banks leading the digital bank charge include:

Citizens Bank: With national aspirations and low brand equity outside of its Northeast and Midwest footprint, Citizens Access offers this high-performing regional a “nationwide digital platform.” Launched in June 2018, Citizens Access had generated $5.8 billion in new customer deposits by the end of 2019. Next up, Citizens is talking expansion into business savings and digital lending.

PNC expanded its digital banking capabilities in October 2018, leading with a high-yield savings account. Like several others, PNC has articulated a “thin network” strategy–combining digital bank investments with lean branch buildout in a few high-opportunity markets (in PNC’s case, Kansas City and Dallas).

Union Bank: Another thin network player, MUFG Union Bank introduced a “hybrid digital bank” under a separate brand, PurePoint Financial, in 2017. With a NYC headquarters setting it apart from Union Bank’s West Coast heritage, the PurePoint positioning emphasizes its parent Mitsubishi’s size and global scale, and its 22 locations in Florida, Texas and Chicago. The requisite high-rate savings and CD offers are complemented with heavy financial education.

Santander Bank recently announced plans for a digital bank later this year, but unlike others, plans to pilot in its Northeast footprint.

Monolines, Specialized Lenders Turn to Digital for Diversification

This category of financial firms includes dedicated credit card issuers with no branch presence (e.g., American Express, Discover), as well as banks with a strong heritage in card or other lending and who have a limited retail banking footprint (e.g., Capital One, Citi, Ally, CIT).

Marketing Priorities and Challenges:

These banks have national lending franchises and strong brand equity. However, as their brands are often strongly associated with their lending operations, a key marketing challenge will be to expand consumer awareness of the bank as a provider of other banking and financial solutions.

They will need to focus on data analysis, targeting, offer development and messaging to effectively cross-sell deposits and other products to their existing card/other loan client bases. This approach will also involve significant cooperation among different business units. Citi has been at the forefront in marketing deposit accounts to its 28 million credit cardholders and generated $4.7 billion in digital deposits in the first 9 months of 2019: two thirds of the deposits came from outside its six core banking markets.

Fintech Disruptors Continue to Emerge

Widespread availability of venture capital and private equity money continues to fuel a spate of fintechs entering the market, including Chime, N26, Radius Bank and Monzo. Many predecessor neobanks have been challenged to achieve scale, as the cost of customer acquisition in digital banking has continued to rise. Fintechs typically partner with a small bank or servicer to offer deposits, but some (such as Varo Money) are now looking for independent bank charters.

Marketing Priorities and Challenges:

The digital bank upstarts tend to appeal to younger age segments who are both more accustomed to using technology to manage their financial needs and less loyal to traditional banks. These companies need to clearly understand how these younger segments consume media and make financial decisions and tailor their marketing investment and messaging accordingly.

As “new kids on the block,” fintechs will need to develop solutions and marketing to differentiate themselves from both traditional banks and other challenger banks.

The design and ongoing review of the digital user experience is critical, as this is the only platform consumers will have to interact with the bank. Some digital banks are not even offering phone-based customer service.

While challenger banks have a number of advantages over traditional banks (such as higher rates on deposits), there are other areas where these newcomers are seen as inferior (for example, a recent Kantar study found that 47% of consumers completely trust traditional banks, but this falls to 19% for challenger banks). Challenger banks need to develop messaging to directly address these areas of vulnerability, and communicate consistently through all consumer touchpoints.

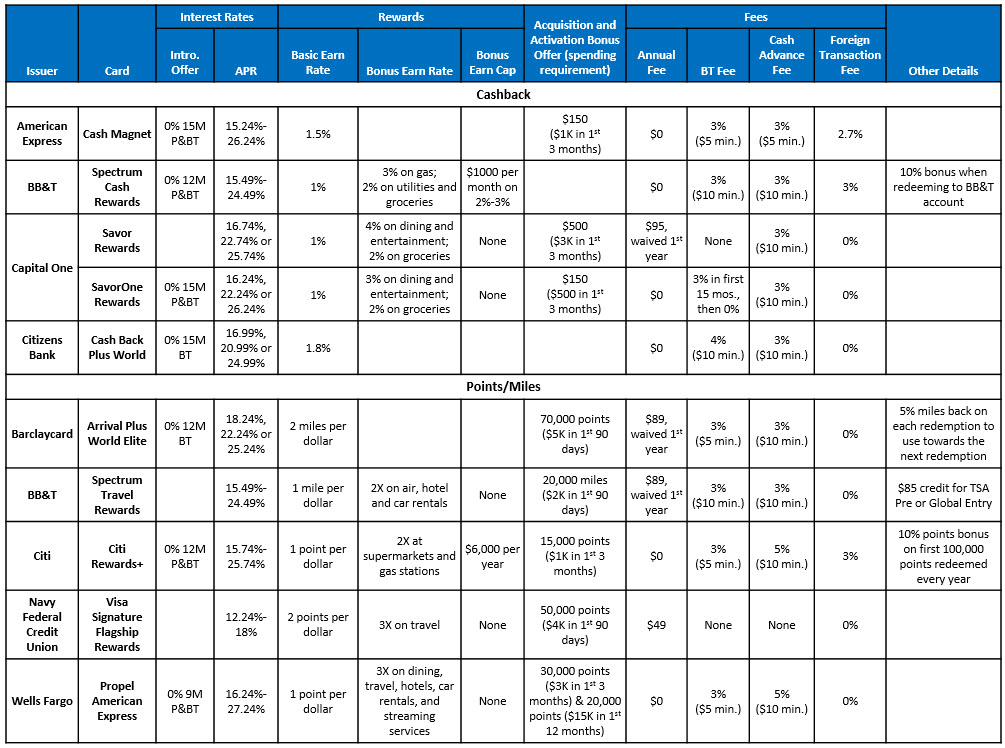

Leading U.S. credit card issuers continued to roll out new credit cards, as they look to attract new clients, cross-sell and upsell existing clients, and win a greater share of clients’ spending.

The following are the common trends or standout elements that we identified among these new cards. (Note that the table at the end of this blog provides a comparison of features/benefits of 10 cards that were introduced over the past 12 months.)

Introductory offers are focused on generating balance transfer volume. 7 of the 10 cards have 0% introductory offers on either purchases and balance transfers or balance transfers only. 6 of these 7 introductory offers have a duration of at least 12 months.

Go-to APRs continue to be prime-based and operate in a broad range. The APR range of many of the new credit cards is at least 7 percentage points. Two cards (American Express Cash Magnet®, and Wells Fargo Propel® American Express) have an APR range of 11 percentage points.

Some cards offer a high earn rate on all purchases. One approach to using rewards to attract and retain cardholders as well as drive more spending is to have an earn rate of more than 1% on all purchases. The Citizens Bank Cash Back Plus® World Mastercard® stands out with an earn rate of 1.8% on all purchases with no limit and no annual fee. The Barclaycard Arrival® Plus World Elite Mastercard® offers 2 miles per dollar on all spending, but carries an $89 annual fee (waived first year).

Issuers continue to offer tiered earning structures. To drive card preference and grow spending in categories where cards have traditionally had a low share, many new cards continue to use tiered rewards structures, with higher earning on categories like travel, gas, dining and groceries. It is worth noting that these bonus earn rates do not come with monthly or annual spending caps.

Acquisition-and-activation bonus offers persist. Issuers continue to promote bonus points/miles/cash back for activating the card and meeting a minimum spend requirement within an initial period (typically three months). Higher-end cards that carry an annual fee also tend to have higher bonus levels. Wells Fargo Propel American Express Card is looking to differentiate itself from competitors with a dual bonus structure: acquisition-and-activation bonus of 30,000 points and an additional 20,000 points for reaching a spending threshold in the first 12 months.

Cards are offering redemption bonuses. Some issuers are looking at rewards redemption as an opportunity to engender loyalty and preference. Cards are offering bonuses:

Most cards have no annual fees, but the cards that do carry an annual fee provide more features, higher earn levels and larger bonuses. Annual fees tend to be waived the first year, although Navy Federal Credit Union’s Visa Signature® Flagship Rewards card has a $49 annual fee and no waiver.

Most cards apply a fee on balance transfers, usually a rate of 3% with a minimum of $5 or $10. Navy FCU’s Visa Signature Flagship Rewards has no BT fees. For its SavorOne℠ Rewards Card, Capital One imposes a fee of 3% during the card’s 15 month introductory period. After this introductory period, there is no fee on balance transfers.

Like BTs, most cash advances come with a fee (of 3% or 5%, with minimums of $5 or $10). Again, Navy FCU stands out with no fee on cash advances.

No foreign transactions fees are quickly becoming the norm, even on non-travel-based cards.