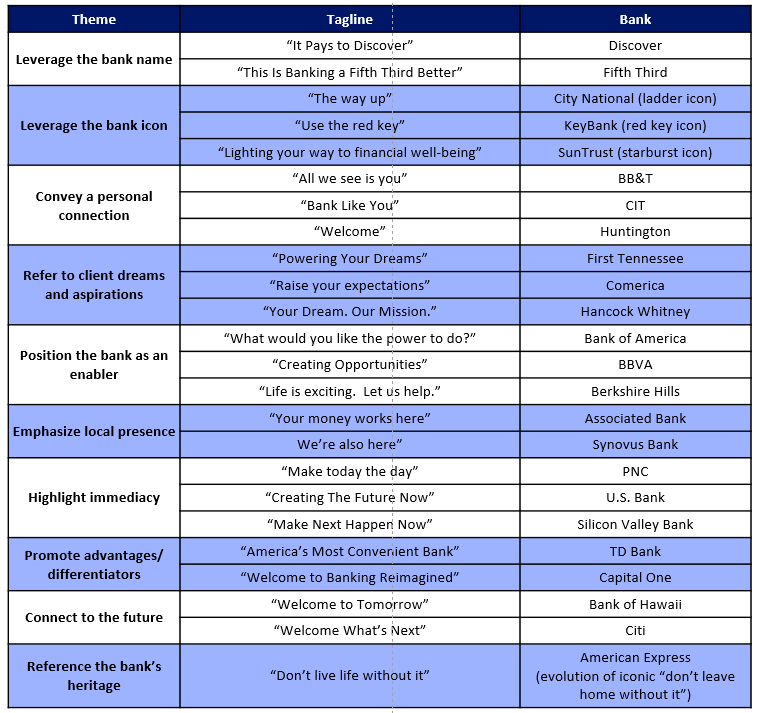

The tagline is an integral part of a bank’s brand identity: it cuts to the core of what the bank aspires to represent for its clients. Banks will typically create a new tagline following a large merger, as an integral element of a major brand overhaul, as part of a new advertising campaign, or even in response to a crisis event.

In creating a new tagline, banks should consider a number of key factors. An effective tagline:

Is short and easy to understand

Is consistent with other bank brand elements

Reflects the bank’s overall positioning and value proposition

Provides themes for advertising and marketing campaigns

With these factors in mind, the following are some themes used by leading U.S. banks in developing their taglines:

Over the past few years, financial institutions have significantly increased their investment in initiatives to grow consumer and small business financial literacy. An even more recent development has been the emergence of workplace-based financial wellness programs: a 2018 survey by Strategic Benefit Services found that 59% of employers offer financial wellness programs or planned to do so. And recent research by Alright Solutions found that 64% of employers say their organization’s financial wellness program is more important now than it was two years ago.

This rise of workplace financial wellness programs has been driven by several factors, including:

The overall growth of investment in financial education programs by the financial services sector in response to concerns about gaps in financial literacy levels, and the proven positive impact that financial education programs have in driving smarter financial behavior by consumers and small businesses.

Employer desire for additional benefits and services to attract and retain staff.

Employee need for financial education: PwC’s 2018 Employee Financial Wellness Survey found that 41% of employees say their employer’s financial wellness plan has helped them get their spending under control.

Recognition of the value and critical role the workplace channel can play in teaching financial concepts, as well as in providing advice and potential solutions.

Financial firms providing workplace financial wellness programs include banks, investment firms, and employee benefits providers. Many of the leading firms in these sectors have launched new or enhanced existing financial wellness programs over the past year:

Principal launched Principal Milestones, which provides personalized information based on an online assessment.

MassMutual introduced MapMyFinances, a financial and benefits planning tool that features a financial wellness score.

Morgan Stanley Wealth Management launched an enhanced Financial Wellness Program for employees of mid-to-large sized corporations, which features a digital portal, a catalog of financial wellness materials, financial assessment as well as the option to collaborate with a Financial Advisor or through Morgan Stanley’s online investing program.

Prudential introduced a range of new financial wellness capabilities, including expanded digital and on-demand solutions, as well as needs-based and life-event solutions.

Unfortunately, financial wellness programs do not tend to be immediately embraced by employees. This can be attributed to a number of factors, including a lack of interest among employees, perceived complexity of the programs, and the lack of resources to manage the program. To overcome these challenges, employers must clearly communicate to employees how they will benefit from engaging with the financial wellness program. To that end, financial institutions need to support employers in marketing the program to employees. It’s also important to gather feedback from employers in order to enhance features and improve the user experience.

The growth in workplace financial wellness programs shows no sign of abating, and we expect financial institutions to further improve and differentiate their programs through new features and options (such as enhancing access to the program via digital channels), as well as continue to develop financial wellness-related content.

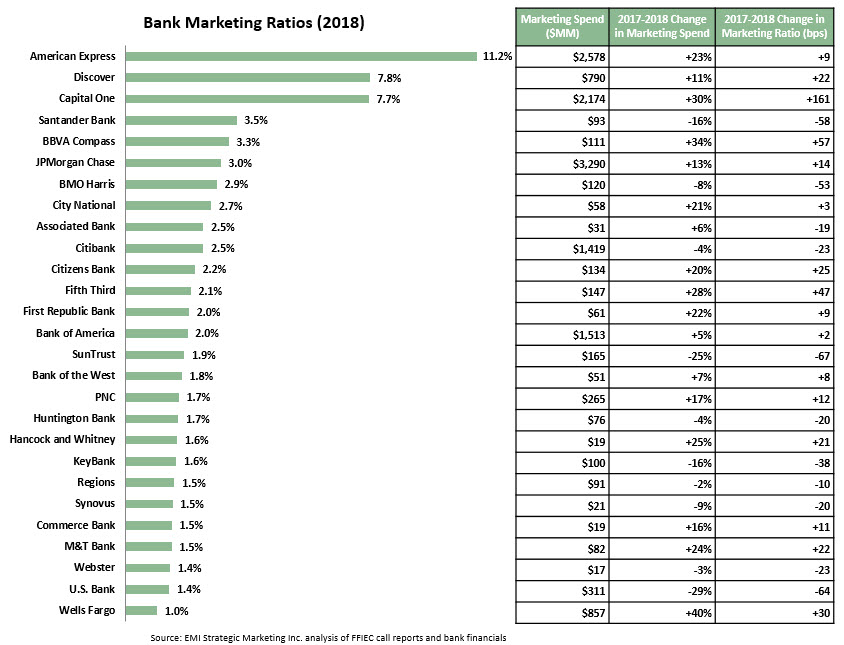

EMI analyzed 2018 marketing spend by 27 of the leading U.S. banks, and found that most banks are ramping up their investment in marketing. The rise in marketing budgets is driven by a number of factors, including:

The continued growth of the U.S. economy.

The ongoing scaling back of bank’s branch networks. This reduces their on-the-ground presence, so banks need to invest more in marketing to maintain brand awareness. In addition, cost savings from smaller branch networks can be redirected to other functions, including marketing.

The need for established banks to reposition themselves in a changing financial services ecosystem, characterized by the emergence of fintech firms and direct (branchless) banks.

Overall, marketing spending by the banks rose 13% to $13.0 billion in 2018.

17 banks grew their marketing budgets.

14 banks increased their marketing spend by double-digit rates, led by Wells Fargo (+40%), BBVA Compass (+34%) and Capital One (+30%).

The 27 banks’ cumulative marketing spend represented 2.9% of their 2018 net revenues, which represents a 17 basis point rise from the banks’ 2017 marketing ratio.

The marketing ratios of the 27 banks ranged from 11.2% for American Express to 1.0% for Wells Fargo.

A majority of the banks (16 of the 27) had marketing ratios in the 1.5% – 2.5% range.

The variation in marketing ratios is due to on a number of factors, including product concentration, size of branch networks, perceived importance of strong brand equity, as well as the timing of marketing investments (such as the launch of new advertising campaigns).

For example, American Express and Discover have no branch networks, are primarily focused on selling credit and charge cards, and have traditionally invested to maintain strong brand awareness. Therefore, their marketing ratios are more in line with fast moving consumer goods firms, rather than financial institutions.

15 banks increased their marketing ratios between 2017 and 2018.

Wells Fargo, which has traditionally had a low marketing ratio as it focused resources of its large branch network, increased its marketing spend by 40% to more than $850 million in 2018, and its marketing ratio grew by 30 bps. The strong rise in spend was in large part due to the launch of the “Re-Established” integrated marketing campaign in May 2018. It is worth noting that Wells Fargo remains well below national bank peers, such as JPMorgan Chase and Bank of America.

Other banks with strong increases in their marketing ratios include Capital One (+161 bps to 7.7%) and BBVA Compass (+57 bps to 3.3%).