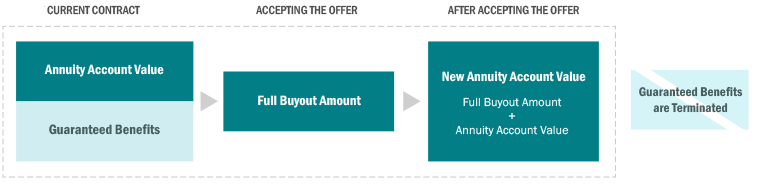

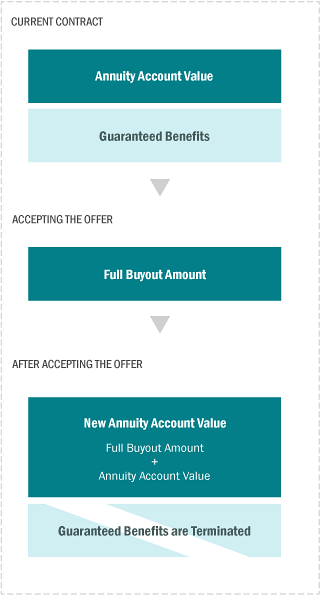

About the Full Buyout Option

AXA Equitable is offering to increase the annuity account value in return for canceling the GMIB and GMDB (and EEB, if applicable). We will also temporarily waive all withdrawal charges for a limited time, so clients can immediately withdraw their account value or transfer or exchange it to another financial product without any charge. At the time of acceptance, applicable prorated charges for the guaranteed benefits will be deducted from the annuity account value, but going forward, all annual charges for those guarantees will no longer apply.

- New Annuity Account Value can be fully withdrawn as cash, transferred or exchanged to another financial product, or it can remain in the contract.

- The New Death Benefit is the Return of Annunity Account Value.

- Applicable prorated charges for the guaranteed benefits will be deducted from the annuity account value at the time of acceptance.

How the Full Buyout Option works

If a client accepts this offer, AXA Equitable will:

- Immediately increase the annuity account value according to the allocation instructions on file. What clients do with the account value is entirely up to them. They will have up to 30 days after the offer expiration to make a cash withdrawal of the new annuity account value without incurring any applicable withdrawal charge. They also have the option to transfer or exchange their contract for a variable annuity with AXA Equitable or another annuity issued by the provider of their choice. Or, they can keep the contract without the guaranteed benefit riders. See the prospectus supplement for details on all available options.¹

- Cancel the GMIB and GMDB (and EEB, if applicable). The standard death benefit will no longer apply. If a death benefit is payable in the future, the amount payable to beneficiaries would be equal to the annuity account value, which could be less than the contributions.

- Deduct prorated annual charges associated with the guaranteed benefits from the annuity account value.

- Stop future deductions of the GMIB and GMDB charges (and EEB charge, if applicable).²

Bear in mind, clients cannot revoke acceptance once we’ve processed it.

¹ The exact amount will depend on the account value and current market conditions when we determine the amount to be added to the annuity contract value. We will determine the actual offer amount and add it to the account on the business day we receive the properly completed acceptance form. If there are any contract transactions on the day we receive the form, the offer amount will be calculated and added on the next business day. For the current offer amount, call 866-638-0550.

² Past GMIB, GMDB and EEB charges will not be refunded. All other contract charges remain unchanged.

Evaluating the offer

This offer can be a great opportunity to meet with your clients, reevaluate their retirement income strategies and reinforce your value as a trusted advisor. To help them navigate this very personal decision, consider the following reasons for why a client may or may not accept the offer.

Reasons for accepting the Full Buyout Option

- Your client has an immediate need for cash now.

- Increasing the account value now is more important than keeping the guaranteed benefits in the future.

- They prefer the flexibility of reinvesting their assets in another financial product better suited to address their new goals.

- They no longer need a guaranteed minimum death benefit.

- They have alternative sources of retirement income and no need for the guaranteed minimum income benefit.

- They no longer wish to pay the charges associated with the guarantees.

Reasons for not accepting the offer

- Their circumstances have not changed since they purchased the original contract, and the reasons that led them to select these guaranteed benefits are still applicable.

- They have no immediate need for cash and no desire to move their assets to another financial product.

- They are relying on the full guaranteed minimum income benefit to fund their retirement.

- They want to leave the full guaranteed minimum death benefit to their beneficiary(ies).

Other important considerations

There are a number of other personal questions that you and your clients should consider as you evaluate the offers.

- Do they expect to keep their contract long enough and live long enough to take full advantage of the guaranteed minimum income benefit?

- Is it still important to your client to bequest a guaranteed minimum death benefit?

- How likely is it that they will change their mind? Guaranteed benefits cannot be reinstated once the offer has been accepted. AXA Equitable may or may not make offers like this in the future.

- How do they expect the market to perform in the future?

- What are the tax implications of accepting this offer?

Options for clients who accept

Upon accepting the Full Buyout Option, clients may choose to:

- Remain invested in the Accumulator variable annuity, continue to let the contract account value accumulate, and take no withdrawals. Their account value will serve as the death benefit.

- Withdraw their full annuity account value. Withdrawal charges will be waived until 30 days after the offer expires.

- Make a partial withdrawal, but still keep a portion of their account value in the contract. As with the full lump sum withdrawal, the withdrawal charges will be waived until 30 days after the offer expires.

- Annuitize the contract so they receive set, periodic payments.

- Transfer all or part of their contract’s account value to another investment product.

- Exchange their contract for another contract issued by the insurance company of their choice. AXA Equitable will allow clients to exchange their contract for a Structured Capital Strategies® Series C or Investment EdgeSM Select contract, as detailed in the Prospectus Supplement. These contracts are not available in all states or through all broker dealers.

Bear in mind, clients cannot revoke acceptance once we’ve processed it.

How we calculate the offer amount

The offer amount for the Full Buyout Option is based on an actuarial calculation of the GMIB and GMDB contract reserves. These contract reserve calculations take into account:

- The owner/annuitant’s life expectancy (based on age and gender).

- The current and projected annuity account value.

- The current and projected GMIB and GMDB benefits.

These calculations are based on large blocks of business, so we do not consider any individual’s health or need for retirement income in making this offer. Because these factors can fluctuate daily, the offer amount will change each business day.

For most contract holders, the offer amount of the Full Buyout Option is the greater of (i) approximately 70% of the actuarial valuation of the GMIB and GMDB reserves; and (ii) two times the GMIB and GMDB fee rate multiplied by the respective current benefit base. We will add an amount equal to two times the EEB fee rate multiplied by the account value.

For those who have withdrawn 25% or more of their annuity account value in any of the three previous full contract years ending on or before June 30, 2015, or in the partial contract year from the most recent contract date anniversary through June 30, 2015, the offer amount will be the greater of (i) approximately 25% of the actuarial valuation of the GMIB and GMDB reserves; or (ii) the GMIB and GMDB fee rates multiplied by the respective current benefit base. If a client has the EEB, the offer amount is increased by one times the EEB fee rate multiplied by the current account value. In general, the offer amount will be less than the difference between the value of the guaranteed benefits and the annuity account value. For more details on how the offer is calculated, review the prospectus supplement.

Why AXA Equitable is making this offer

The offer can be mutually beneficial to some contract holders and AXA Equitable. Contract holders whose financial needs have changed since they purchased the guarantees may have greater need for flexible access to their assets now than for maintaining future income guarantees. At the same time, AXA Equitable benefits because ongoing low interest rates make maintaining these benefits costly to us, and the credit amounts we are offering to clients are less than the amounts we’re currently setting aside to guarantee the benefits.

Details on AXA Equitable's financial strength ratings.